We are on record for recommending that defined contribution plan (DCP) fiduciaries monitor active management using a three-year performance window and replacing all underperforming active managers with passive alternatives immediately. Having passive funds representing each asset class enables more straightforward asset allocation targeting for participants and greatly reduces the fiduciary oversight burdens and costs. To evaluate this approach, we performed an analysis of comparing two universes of investments. One is a universe of all active funds and the other is a universe of active funds being replaced with passive alternatives in the month following a 3- or 5- year underperformance period. This is to simply examine whether plan participants and fiduciaries would be better served with a switch to passive rather than trying to replace active managers with other active managers. Most fiduciaries are ill prepared to be able to identify consistently outperforming active managers. They would better serve their constituents by using passive exposures to each asset class rather than play this losers game. Many fiduciaries indefinitely postpone the decision resulting in wealth loss to plan participants.

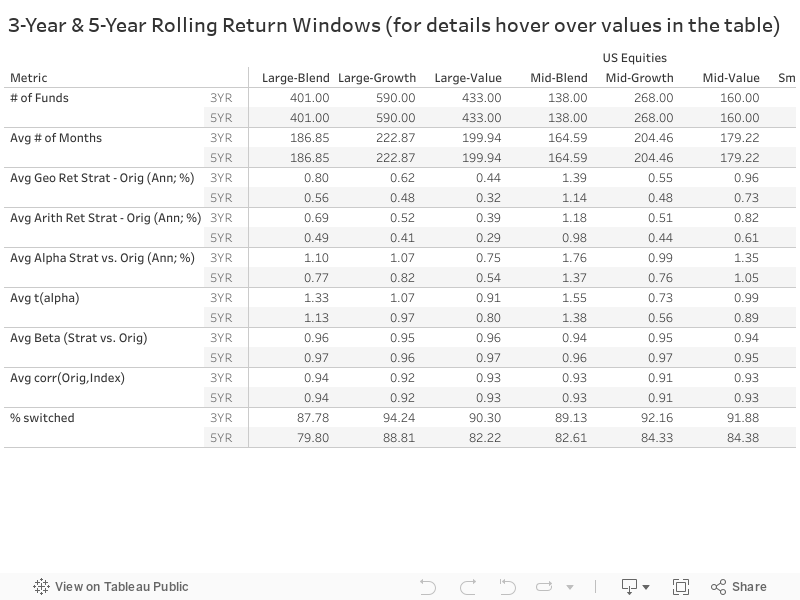

Our results match our expectations. We use the entire Morningstar mutual fund universe to evaluate our hypotheses. We divide the US equity space along the lines of the 3X3 style/blend categories and use the Russell equity indices for each style cell to evaluate performance. Our results are presented below and confirm that all parties involved in the DCP process would be better served by replacing active equity funds with passive alternatives across the US equity space. Additionally, using the 3-year performance window better serves plan participants than using a 5-year performance window. Delaying replacement decisions only loses wealth.

A common academic criticism of using a performance threshold to trigger active fund replacement is that it lacks statistical significance and that any fixed investment window is never long enough. The cringe worthy term market cycle is often deployed to build a defense for effectively any performance related replacement discipline. This creates an environment where fiduciaries never have to make a replacement decision. It is a convenient legal construct that absolutely fails to take the best interest of plan participants into consideration. From our perspective these are all nonsensical. Our previous results clearly show that plan participants are better off by replacing underperforming active managers with appropriate passive funds. And the sooner this is done the better for the investor. To suggest that statistical significance and a longer investment window is required only destroys wealth. Again, the party that loses in this framework is the individual investor (plan participant). We now turn to show this empirically.

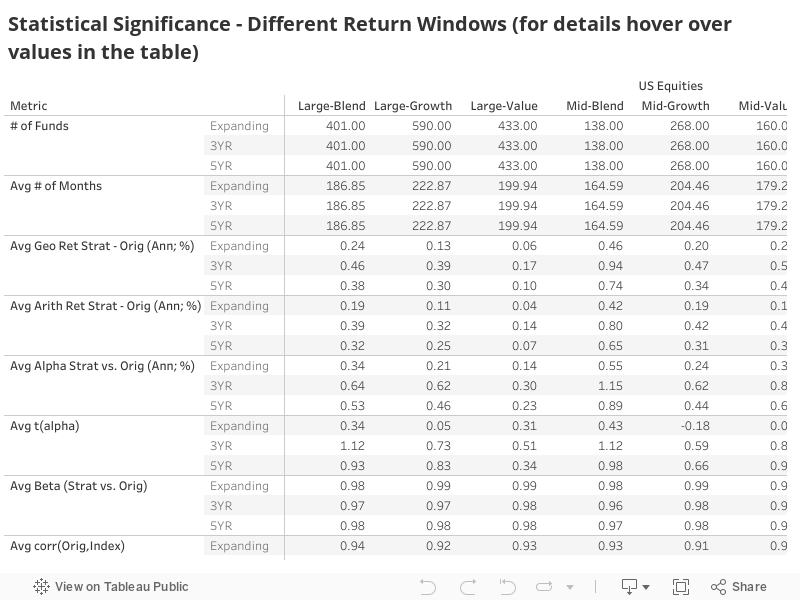

Before we present our results, let’s review what statistical significance really measures in this context. Statistical significance is measured using the quotient of outperformance to the standard error of that outperformance metric. It can be the result of a properly run regression or simply evaluating a time series of excess returns. If the benchmark used is correct, then either approach is reasonable. The quotient contains a linear numerator (average) and a non-linear (square root) denominator. Thus, the quotient is generally more impacted by the numerator and generates an interesting characteristic. If the random variable being evaluated (outperformance) contains the property of reverting to the mean (zero), then the numerator will gradually approach zero as the period increases. Since it is linear it will also revert faster than the non-linear (square root) denominator. Thus, while academics argue for statistical significance and longer investment windows, they essentially are creating a framework that will rarely produce a replacement trigger. This creates what we call the fiduciary paradox. By arguing for longer periods and statistical significance the fiduciary will rarely have to make a responsible replacement decision. Our results below show this to be the case as the expanding investment window has by far the lowest replacement percentages. Even this flawed approach adds value relative to simply remaining invested in the active funds regardless of their performance. However, the added value is only a fraction of our earlier results.

We also include the results for the 3-year and 5-year trailing windows. Instead of replacing active with passive investments as soon as they underperform, we also require statistical significance of the performance measure. Due to the active to passive replacement dynamic, these results are an improvement over the expanding window results but not nearly as beneficial as our original results. It seems that those promulgating the fiduciary paradox create an environment of wealth destruction for plan participants. Moreover, all our results clearly show that the active to passive replacement framework creates the best outcome for plan participants.